Research Brief: Multifamily October 2022

Housing Supply Action Plan Becomes More Concrete; Market Normalization Underway

October 2022

Excerpt of Full Report:

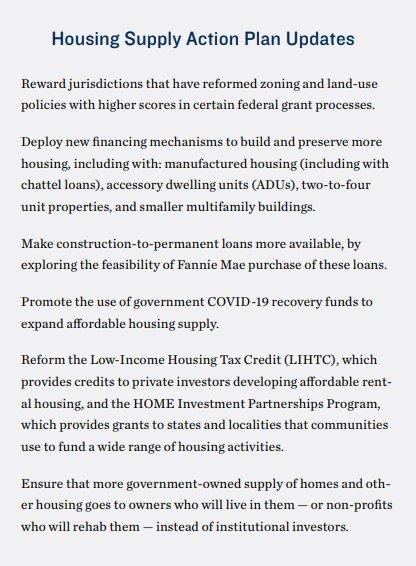

White House aims for greater housing affordability. Incentivizing the construction of lower-income housing in various forms is the primary goal of the Housing Supply Action Plan, updated this October. In particular, a proposed income averaging provision for the Low-Income Housing Tax Credit would make development more feasible in sparsely-populated areas, by no longer requiring all tenants to meet the same income threshold. This change joins a series of other alterations and additions, designed to ease the regulatory and financial hurdles of building income-restricted dwellings. Addressing housing affordability is becoming a priority for the Biden administration, after steep home price run-ups directed excess demand to apartments and drove up rental costs

Economic uncertainty weighing on apartment demand. Following the strongest first quarter on record for multifamily net absorption earlier this year, the metric has now dipped negative in consecutive three-month spans. National vacancy rose from just 2.4 percent in March to 4.1 percent in September. For a historic context, this rate is about 120 basis points below the same month’s average between 2000-2019, but up by the same 120-basis-point margin from one year ago. This indicates a normalization is playing out, after a stretch of historically tight conditions. Fewer people are forming new households amid broad-based uncertainty, hindering rental demand. At the same time, new supply is being delivered at a blistering pace, creating a temporary imbalance.

Rent growth settles. The average effective apartment rent in the U.S. was up by a double-digit percentage year-over-year in the third quarter, but the pace is easing as availability increases and units take longer to fill. In September, rentals in the U.S. remained vacant for 27 days on average, up from 23 days in the same month of 2021. This is producing smaller rate adjustments for new tenants. Rent increases for units leased out to new occupiers dropped from a 2022 peak of 19.1 percent in May to 11.3 percent in September. Meanwhile, rates for tenants renewing their leases have climbed throughout this year, as rents are realigned to the market, following significant upward movement over the past 18 months.

Denver Office:

Adam Lewis Vice President, Regional Manager

Tel: (303) 328-2000 | adam.lewis@marcusmillichap.com

Prepared and Edited By:

Benjamin Kunde Research Analyst | Research Services

For Information on national multifamily trends, contact:

John Chang Senior Vice President, National Director | Research Services

Tel: (602) 707-9700 | john.chang@marcusmillichap.com

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or reliability of the information contained herein. Note: Metro-level employment growth is calculated based on the last month of the quarter/year. Sales data includes transactions sold for $1 million or greater unless otherwise noted. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Real Capital Analytics; RealPage, Inc. © Marcus & Millichap 2021 | www.MarcusMillichap.com