National Report: Multifamily 2Q/23

Ingredients in Place for Long-Term Growth As Sector Adapts to Recent Headwinds

Excerpt of Full Report:

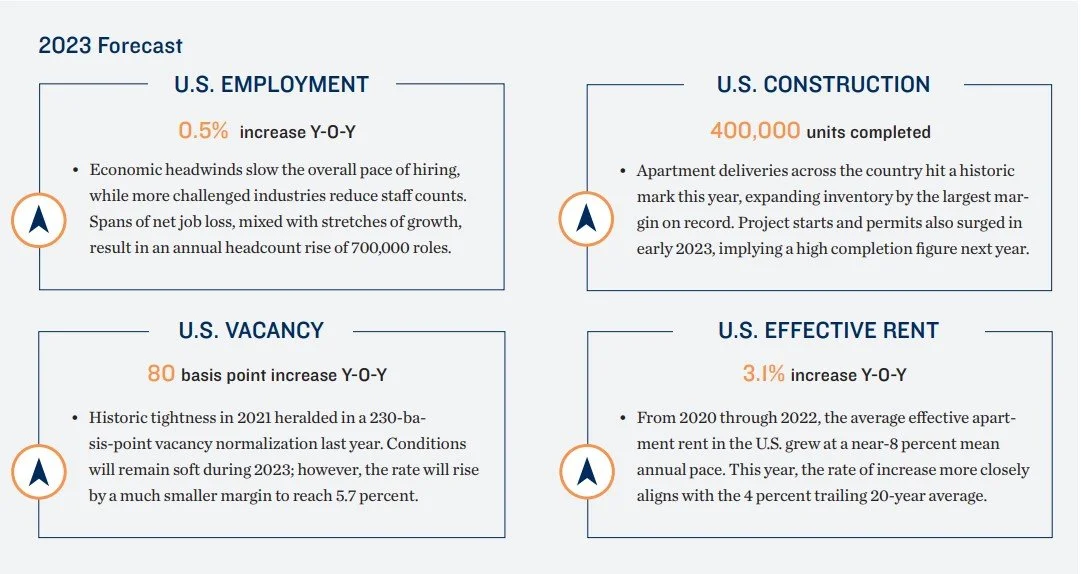

Fundamentals continue to soften as the economy cools. After hitting an all-time low of just 2.5 percent in early 2022, apartment vacancy in the U.S. has now risen in four straight quarters. Availability surpassed the 5 percent mark in March, the fi rst time it has eclipsed that threshold since 2018. From a historical context, however, vacancy is on par with the trailing 30-year average. Higher availability nevertheless has fl attened rents, following record-setting growth during the pandemic. As of the fi rst quarter of 2023, the average eff ective monthly rate nationally was down about 0.6 percent from 2022’s peak, but still up 6.4 percent year-over-year. Immense new supply over the remainder of this year will keep vacancy on an upward path near-term, while also lifting the average rent as new high-quality units come online. The potential for supply overhangs in select markets with large pipelines is likely, yet population and housing dynamics indicate that these deliveries are necessary longer-term.

Pent-up household creation will propel sector. The share of young adults living with parents surged to new heights during the pandemic amid unique work and education arrangements. That fi gure has since ticked down, but economic headwinds and infl ation are now further stunting household creation in this cohort. Once more young adults gain the fi nancial confi dence to move out on their own, pent-up household formation will release, aiding rental demand. Meanwhile, millennials are remaining renters for longer amid homeownership barriers, and immigration is trending up, brightening the outlook.

Supply Pressure Detectable in Some Markets, but Appetite for New Units is Improving

Supply Trends

More than 950,000 units were underway across the U.S. entering the second quarter of 2023. Roughly 400,000 rentals are expected to fi nalize throughout the duration of this year, equating to the largest annual delivery volume on record and implying the 2024 slate will also be substantial. Despite some fundamental softening in recent quarters, multifamily project permits rose during early 2023 as well. This reflects developer confidence in the sector’s long-term outlook

Construction is largely concentrated in a handful of Sun Belt markets with strong foundations for sustained long-term economic growth. Dallas-Fort Worth, Phoenix, Austin, Houston and Atlanta combine for over one-fourth of the units underway nationally. These same metros are also expected to comprise nearly 20 percent of the country’s total household creation over the next fi ve years. Job availability, cost-of-living and quality-of-life considerations will maintain these metros’ appeal as top migration destinations.

The list of metros projected to have smaller inventory growth in 2023 relative to last year is thin, but includes several of the nation’s largest markets. New York, San Francisco, Oakland, San Jose and Seattle-Tacoma will all have reduced inventory growth in 2023. These were some of the harder-hit areas during the pandemic, yet remain among the most compelling places for young professionals to reside

Demand Trends

Net absorption turned positive during the opening quarter of this year, following three straight negative measures from April through December 2022. While the fi gure was below apartment completions, keeping vacancy on an upward path, the tides may be shifting. During the final nine months of this year household creation is expected to tick up, allowing annual absorption to surpass 200,000 units.

Seven major U.S. markets posted year-over-year vacancy rises exceeding 350 basis points in March, all of which are located in the Sun Belt and performed exceptionally well during the pandemic. Tucson, Phoenix, San Antonio and Las Vegas had the most extreme jumps in availability, as the fast pace of building in these metros outstripped softer demand. For similar reasons, Dallas-Fort Worth, Austin and Jacksonville also had sizable vacancy elevations

Only two major markets registered year-over-year vacancy declines — Northern New Jersey and San Francisco — which have slightly diff erent dynamics. Northern New Jersey is benefi ting from remote work models still prevalent in the Northeast region, as workers can opt for cheaper living costs here. Meanwhile, San Francisco is gradually undergoing a delayed recovery from the pandemic. The construction pace here has also settled, helping reduce availability. New York logged a minimal vacancy increase due to similar characteristics.

Population Dynamics Amid Homeownership Challenges Should Keep Investors Tuned In

2023 INVESTMENT OUTLOOK

Capital markets environment continues to press on deal flow. After apartment asset sale prices surged in 2021 and the first half of 2022, which correspondingly compressed cap rates to historic lows, the rapid interest rate increases that followed have created pronounced challenges. Tight cap rates placed yields in a difficult position to move deals forward, as the margin between implied returns and debt service costs became unfavorable. Institutions have largely remained on the sidelines taking a wait-and-see approach, while some private investors are taking advantage of a potential window of opportunity amid reduced competition from the buyer side.

Prices and cap rates reflect changing landscape. A general slowdown in the transaction market, alongside private buyers accounting for a larger share of overall deal flow, is influencing sales metrics. The average cap rate on assets traded during the trailing year ended in March rose 40 basis points to 5.1 percent, while the mean sale price fell roughly 5 percent to $196,000 per unit.

Massive pipeline represents the future of the transaction market. With nearly 1 million units underway across the country entering the second quarter, the next few years will include a barrage of new supply. These deliveries may present investment opportunities and development partnerships to institutions and well-capitalized buyers. Private investors could fi nd upside in older properties in areas where new supply lifts market rents, or in well-located assets rooted in neighborhoods where development is less practical.

Less Assertive Monetary Policy Tightening Could Help Alleviate Transaction Hurdles

Federal Reserve enacts 10th rate hike in 14 months, indicates increased caution going forward. The Federal Open Market Committee lifted the federal funds rate by 25 basis points at the March meeting and subsequently did the same on May 3, marking the third upward adjustment of that scale this year and moving the lower bound to 5.00 percent. Prior to the March rate hike, the market was anticipating a 50-basis-point increase, but the seizures of Silicon Valley Bank and Signature Bank prompted caution. Nevertheless, the Fed remains intent on curbing infl ation and cooling the job market, making their future actions a balance of several dynamics. Core CPI inflation remained above the target range in March at 5.0 percent, but the metric has come down considerably from the 9.1 percent peak recorded last June. The Fed’s preferred measure, Core PCE, has also declined in four of the last fi ve months through February. Meanwhile, the labor market has been resilient despite higher debt costs, with the U.S. adding 800,000-plus jobs in eight straight quarters through March to produce a headcount that tops the pre-pandemic peak by over 3 million roles. If the FOMC suspended future rate hikes, the interest rate stability would allow buyers to better work with sellers and capital providers, aiding multifamily deal fl ow

Lenders remain active, but with heightened due diligence. Multifamily’s proven track record, crucial role in the nation’s housing landscape, and strong outlook amid homeownership barriers instill a level of confidence in the sector. Conventional lenders, as well as agencies like Fannie and Freddie, remain engaged despite hurdles. The recent treasury rate softening is allowing financiers to better navigate the environment, though many are utilizing an artificial rate floor. Some stress in the banking sector that emerged during the first quarter is likely to result in a general lending pullback and prompt increased due diligence, but agencies have capital available and should serve as a backstop. Nonetheless, LTV’s may be heavily scrutinized, and lenders could take more conservative underwriting and debt service coverage approaches. These current challenges, however, do not deduct from the medium- to long-term value proposition of apartments. The sector is well-positioned amid homeownership hurdles and pent-up household formation, while ongoing valuation adjustments are marginal relative to the sector’s 70-plus percent average sale price growth across the past decade.

Denver Office:

Adam Lewis Vice President, Regional Manager

Tel: (303) 328-2000 | adam.lewis@marcusmillichap.com

Prepared and Edited By:

Benjamin Kunde Research Analyst | Research Services

For Information on national multifamily trends, contact:

John Chang Senior Vice President, National Director | Research Services

Tel: (602) 707-9700 | john.chang@marcusmillichap.com

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or reliability of the information contained herein. Note: Metro-level employment growth is calculated based on the last month of the quarter/year. Sales data includes transactions sold for $1 million or greater unless otherwise noted. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Real Capital Analytics; RealPage, Inc. © Marcus & Millichap 2021 | www.MarcusMillichap.com