Special Report: Natural Disasters and Insurance Risk

Hurricane Idalia and Other Weather Events Have Potential to Transform Investment Landscape

Insurance expenses accelerate. Hurricane Idalia made landfall in late August on Florida’s Gulf Coast as a Category 3 tropical cyclone. Idalia brought violent winds, rain and flooding to the region, before hitting Georgia and the Carolinas. The storm surge displaced communities and significantly damaged personal and commercial real estate assets, along with public infrastructure. While the total cost is still being assessed, Idalia occurred just 11 months after Hurricane Ian caused $112 billion in damages to nearby communities southwest of Idalia's landfall. Beyond the impact to real estate, these and other dangerous weather events have placed meaningful financial risk on living, working and investing in areas subject to extreme climates. Attempting to account for the increasing frequency and impact of natural disasters, insurers have drastically raised premiums over the past few years in states like Texas, California and Florida. Influenced by Hurricane Ian, the average per-unit cost of multifamily insurance across Jacksonville, Tampa-St. Petersburg, Orlando and Miami-Dade climbed by more than 38 percent year-over-year in June. These rates are likely to accelerate further here, as well as in other cities affected by Hurricane Idalia, including Charleston, Wilmington and Savannah.

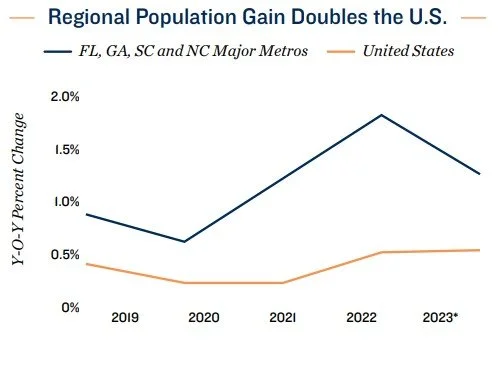

Southeast's population surge may begin to normalize. Even before Idalia's impact on insurers in the region, estimated single-family premiums in Florida had already risen to $6,000 per year. The expense, which is nearly four times the U.S. mean, may weigh on the future pace of net in-migration — a key driver for economic growth in the southeast region and an appealing factor for property investment. Of the 10 major metros with the strongest net in-migration from 2020 to 2022, half were located in the Carolinas, Georgia or Florida. In the retail sector, the population-induced upgrade to local consumer spending helped propel average asking rents up by more than 18 percent in metros like West Palm Beach and Jacksonville over the span. However, more expensive housing costs — exacerbated by elevated mortgage rates and climbing homeowners' insurance — may soften this trend moving forward. As this dynamic unfolds over time, the character of commercial real estate investment opportunities in the region may change.

Expense-pressured owners may be more inclined to sell. An ongoing climb in insurance costs may stir listings from owners facing tighter margins. This could spark deals among sellers looking to capture proceeds from recent price appreciation and well-capitalized buyers increasing their regional holdings. In the multifamily sector, mean per-unit prices across each major metro in the Carolinas, Georgia and Florida over the year ended in June were up by at least 30 percent over the 2019 mark. Still, regional deal flow may remain subdued. Prospective buyers may underwrite conservatively to properly absorb rising insurance costs, which could place upward pressure on yields and hinder deal-making. Meanwhile, some institutional funds that primarily target the southeast may diversify away from coastal markets to reduce risk.

Growing Prevalence of Natural Disasters Increasingly Influence Investor Strategies.

Natural disasters rise in frequency. Hurricane Idalia was this year's 16th extreme weather event with more than $1 billion in property damages. The pace set so far in 2023 has already nearly matched the trailing three-year average of 20 events, which in itself is up from a mean of 12.8 in the 2010s. Extreme weather is also becoming more geographically widespread, as many natural disasters have recently hit central and mountainous states, rather than just the southeast. Along with hurricanes, other forms of climate disasters, such as flooding and wildfires, have plagued states like California, Washington, Oklahoma and Oregon. For some owners, this has presented significant risk. Even if insurance covers the cost of repairs to damaged properties, investors are still impacted by interrupted cash flows and other logistical hurdles. At the same time, to cover the frequency and cost of weather events, insurers are having to raise premiums for properties, which in turn impacts investors' decision-making.

Mounting home insurance props up multifamily demand. Nationally, homeowners' insurance jumped by 12 percent year-over-year, emphasizing ownership barriers already presented by elevated mortgage rates. This rising expense for home buyers underscores the relative cost benefit of renting, with the national difference between the average monthly mortgage payment and the mean apartment rent eclipsing the $1,000 mark for the first time in September 2022. Nevertheless, the average per-unit cost of multifamily insurance went up by 33 percent annually, which was almost triple the single-family rate. While the higher cost will not be directly passed on to renters, owners will generally be forced to grapple with tighter margins in states that are at risk for climate disasters. Geographic diversification, as a strategy to mitigate rising expenses, may be increasingly adopted by investors across the property spectrum, in an attempt to unwind cash flows from locational dependency.

Investors may spread out portfolios to mitigate risk. Market familiarity, local relationships, and access to sales comparable often drive buyers to focus on specific metros, states or regions. However, the growing prevalence of natural disasters will place greater emphasis on geographic diversification to reduce long-term risk. In the multifamily sector, per-unit insurance as a percentage of owners' total expenses rose beyond double digits in coastal metros like Miami, Tampa, Jacksonville, Houston and Los Angeles. In the first half of 2023, these markets accounted for over 16 percent of national apartment trades. Investors that target such metros could bolster their holdings by additionally acquiring assets in areas with less climate risk. Over time, this may lead to a more geographically-dispersed investment landscape. The growing unpredictability and impact of climate events will give owners greater motivation to spread out their portfolios beyond the metros that they are currently familiar with.

Denver Office:

Adam Lewis Vice President, Regional Manager

Tel: (303) 328-2000 | adam.lewis@marcusmillichap.com

Prepared and Edited By:

Benjamin Kunde Research Analyst | Research Services

For Information on national multifamily trends, contact:

John Chang Senior Vice President, National Director | Research Services

Tel: (602) 707-9700 | john.chang@marcusmillichap.com

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or reliability of the information contained herein. Note: Metro-level employment growth is calculated based on the last month of the quarter/year. Sales data includes transactions sold for $1 million or greater unless otherwise noted. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Real Capital Analytics; RealPage, Inc. © Marcus & Millichap 2021 | www.MarcusMillichap.com