Special Report: Financial Markets Banking Shock Response

Bank Closures Spur Capital Markets And Federal Reserve Recalibration

Excerpt of Full Report:

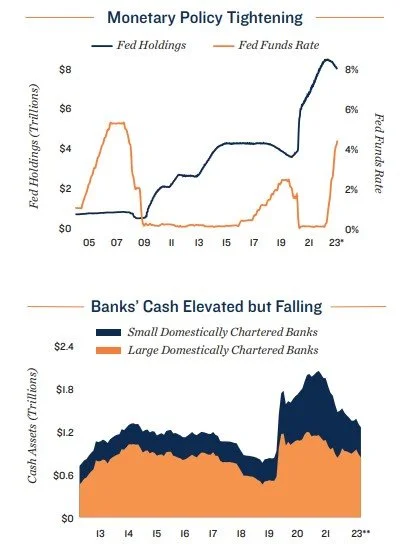

Banking turmoil may encourage the Fed to tread carefully. Over the past year the Federal Reserve has aggressively increased interest rates in a bid to cool infl ation, creating challenges for commercial real estate investors and lenders. Messaging from the Fed prior to the recent bank failures implied that they would remain assertive, but the high-profi le collapses could encourage a more cautious stance. While the banking sector’s stress rippled across capital markets and prompted many lenders to widen their spreads, the higher probability of more stable rates in the near term could serve as a positive for real estate transactions. Government agencies have also been quick to respond, soothing concerns that a broader contagion will occur.

Regulators seize the nation’s 16th-largest bank. On March 10, California state regulators placed Silicon Valley Bank (SVB) into FDIC receivership, marking the largest banking collapse since 2008. Two days later, New York authorities closed Signature Bank for irregular practices. The bank was also heavily engaged with clients in the beleaguered cryptocurrency sector. While both institutions faced similar underlying troubles, each collapse was independent of the other. The chain of events leading up to these failures extends to the pandemic. Tech companies did very well during that time, leading to heightened infl ows of deposits into SVB, which is a prominent fi nancier of the sector. Needing a place to store all this cash amid excess liquidity, the bank allocated a large portion of its capital base to securities and long-term U.S. treasuries. Most of this was done prior to the Federal Reserve’s rapid series of interest rate hikes, thus the value of those government bonds dropped as rates increased, producing paper losses. Those unrealized erosions would not have been problematic, however, if tech-industry specifi c headwinds did not prompt a wave of fi rms to withdraw funds, placing immense pressure on SVB.

Tech sector stress put SVB in a difficult position. The technology industry, especially startups that grew at an unsustainable pace during the pandemic, have been among the most visibly impacted in recent quarters. Layoff s have been much more common in the sector relative to other labor segments, while the initial public offerings market and fundraising also slowed down drastically. This coaxed some tech industry firms to withdraw funds from banks like SVB to meet their liquidity needs. As a result, SVB was forced to sell a $21 billion bond portfolio before maturity and incur a $1.8 billion loss to help fund the wave of withdrawals. This activity ignited a powder keg that ultimately led to the bank’s demise.

Spiral of events quickly led to a collapse. Trying to cover the losses from the bond portfolio sale, SVB attempted to sell $2.25 billion of common equity and preferred convertible stock. This announcement backfired, however, spooking additional clients into withdrawing funds. Investors also responded to the news by selling off SVB parent company stock, further hampering the bank. Amid this freefall, SVB unsuccessfully tried to sell itself on March 9, leading additional clients to withdraw funds and sending the stock price even lower. One day later, financial regulators stepped in and shut down the bank. In the following days, the federal government quickly responded to quell fears of a broader financial market contagion event.

Federal Government Agencies Spring to Action to Suppress Contagion Risks

The banking sector is more stable than in 2008. Federal agencies have been quick to respond to SVB and Signature Bank’s failures, in order to curtail fears that they will be the fi rst in a series of dominoes to fall, like Bear Stearns, Lehman Brothers and Washington Mutual in 2008. The circumstances, however, are much diff erent now than they were at the kickoff of the global fi nancial crisis. Both SVB and Signature Bank had heavy exposures to certain industries that are going through challenging times. Most other similarly-sized banks are more diversifi ed, mitigating that risk. Additionally, regulatory reform after the 2008 fi nancial crash has created a more stable banking industry in general. While many other banks with excess liquidity during the pandemic also put funds into U.S. treasuries and bonds when interest rates were historically low, those unrealized losses will not pose a problem, unless a wave of depositors rush to withdraw. Federal agencies have taken action to shore up protections in the aftermath of SVB and Signature Bank’s collapse and avoid contagion.

Lending program headlines response measures. Silicon Valley Bank provided fi nancing for a considerable share of venture-backed tech and health care fi rms in the U.S. This idiosyncratic corporate client base meant that more than 85 percent of the bank’s deposits were uninsured, as they exceeded the $250,000 threshold. Following the collapse, the U.S. Treasury used the systemic risk exception to instruct the FDIC to make whole with all depositors, including the uninsured. The support will not come from taxpayer funds, but rather from a variety of programs, including a special assessment on all banks and the Federal Reserve’s reverse repo facility. To address problems that could arise in the broader banking sector moving forward, the Fed introduced a Bank Term Lending Program (BTLP). Financial institutions pressured by the drop in bond prices and needing a BTLP loan can use collateral assets at par, instead of being marked to market. This source of liquidity should help banks with similar bond value challenges to SVB avoid facing the same fate..

Some smaller-sized banks still face uncertain futures. The BTLP should alleviate the need for a stressed bank to abruptly sell securities at a loss. Allowing collateral assets at par also means that depreciated bond values should not hinder the amount that a bank can borrow, including from the Fed’s discount window. Still, it is estimated that U.S banks held about $620 billion in unrealized losses at the end of 2022, leaving the near-term outlook uncertain for some institutions with smaller balance sheets. Irrational public fears leading to additional bank runs would put strain on the fi nancial industry. Although, the rapid and expansive measures taken since SVB’s collapse should allow most banks to weather some choppy water.

Banking Shock Ripples to Broader Capital Markets with Mixed Impacts

Lenders become slightly more conservative post-SVB collapse. Many banks have already adopted more caution over the past few quarters, and the recent fi nancial sector turmoil may further heighten due diligence. While the SVB and Signature Bank seizures were a consequence of unique circumstances, lenders across the industry will likely heavily scrutinize LTVs and take conservative underwriting and debt service coverage approaches. Reducing their risk profile may be paramount for depository institutions as regulators pay closer attention to balance sheets. Meanwhile, a fl ight-to-quality has pushed down interest rates on vehicles like treasury bills, but lenders have also widened their spreads. This combination should have a relatively negligible impact for borrowers

Commercial real estate borrowers face some extra hurdles. As many lenders tighten underwriting in response to the bank seizures and greater regulatory attention, commercial real estate borrowers may have some additional obstacles to combat. Interest rate increases over the past year have made debt service coverage tests a significant constraint on the amount of leverage available for refinancings and new loans. Many lenders will require borrowers to pay down some of their existing loan if they want to refi nance. Additionally, most banks will continue to focus on standing relationships rather than growing their books. This is partially due to liquidity constraints enforced by high short-term bond yields, as depositors shift funds to those instruments. These dynamics will sustain real estate transaction hurdles near term and keep buyer-seller expectations separated. Nevertheless, opportunities are still out there for investors who do not need a lot of leverage. Agency lenders like Fannie and Freddie may also serve as a good option for some borrowers, as they have ample liquidity and remain active.

Bank failures pose minimal risk to real estate outlooks. The turbulent banking sector events have not distinguished underlying operating fundamentals and long-term outlooks for commercial real estate. The nation is still facing a housing crunch amid substantial barriers to buying a single-family home, supporting apartment demand. Industrial and retail also proved resilient during the pandemic and entered 2023 in strong positions, while self-storage was another standout performer that should be able to weather any upcoming headwinds. Pent-up demand for travel and vacations also propelled the hotel sector’s recovery, exceeding historic performance averages last year. Demographic trends signal robust demand for senior housing and medical offi ce services in the coming decade as well. Outside of the beleaguered offi ce segment, the prospects supporting commercial real estate remain robust and should keep investors tuned in

Fed’s Interest Rate Decision is a Balance of Several Moving Factors

Bank failures could coax the Fed to advance more cautiously. While the Federal Reserve has indicated they want to avoid prematurely ceasing monetary policy tightening, the collapse of SVB and Signature Bank could alter their path forward. The market had been widely anticipating a 50-basis-point increase to the benchmark rate at the March 22 meeting, but the banking sector events that transpired earlier this month have since tempered expectations. Projections now favor a 25-basis-point lift, matching the February adjustment, or even holding the rate fi rm. Rapidly rising interest rates over the past year contributed to SVB’s demise by lowering the value of their bond portfolio. Other financial institutions are facing a similar reality in terms of unrealized losses, giving the Fed a signal that their aggressive monetary policy tightening is working its way through the system. A pullback in lending may also help slow the economy. At the same time, job creation has been robust and inflation remains above the target range, making the decision a nuanced one for the Fed.

An unsullied labor market leaves the Fed unsatisfied. Intentions by the Federal Reserve to cool the nation’s employment market have been largely unsuccessful up to this point. Through February 2023, jobs have been added on net in the U.S. for 26 consecutive months, now surpassing the pre-pandemic peak headcount by almost 3 million personnel. At the same time, recent labor market updates have provided some early signs of a potential softening. Participation in the prime working-age population group is trending closer to prehealth crisis norms, while wage growth is beginning to slow down. These considerations will be taken into account by the Fed as they decide the best path forward to subdue persistent inflation.

Inflation pace is settling, but still triples the FOMC target. Headline CPI rose by 6.0 percent year-over-year in February, which was the smallest elevation since September 2021. While this rate remains significantly higher than the Fed’s target of 2 percent, the slower pace of price increases should serve as a positive sign that inflation is settling. Conversely, core CPI ticked back up in February after decelerating across several prior months, an indication that inflation may not yet be completely under control. Continued progress in stunting upward price pressures will remain a key determinant in shaping the Fed’s plans at upcoming meetings.

Denver Office:

Adam Lewis Vice President, Regional Manager

Tel: (303) 328-2000 | adam.lewis@marcusmillichap.com

Prepared and Edited By:

Benjamin Kunde Research Analyst | Research Services

For Information on national multifamily trends, contact:

John Chang Senior Vice President, National Director | Research Services

Tel: (602) 707-9700 | john.chang@marcusmillichap.com

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or reliability of the information contained herein. Note: Metro-level employment growth is calculated based on the last month of the quarter/year. Sales data includes transactions sold for $1 million or greater unless otherwise noted. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Real Capital Analytics; RealPage, Inc. © Marcus & Millichap 2021 | www.MarcusMillichap.com