Market Report: Multifamily Denver Metro Area

High Incomes Allow for Metrowide Improvements Amid Demand Shift Back into Urban Core

April, 2022

Excerpt of Full Report:

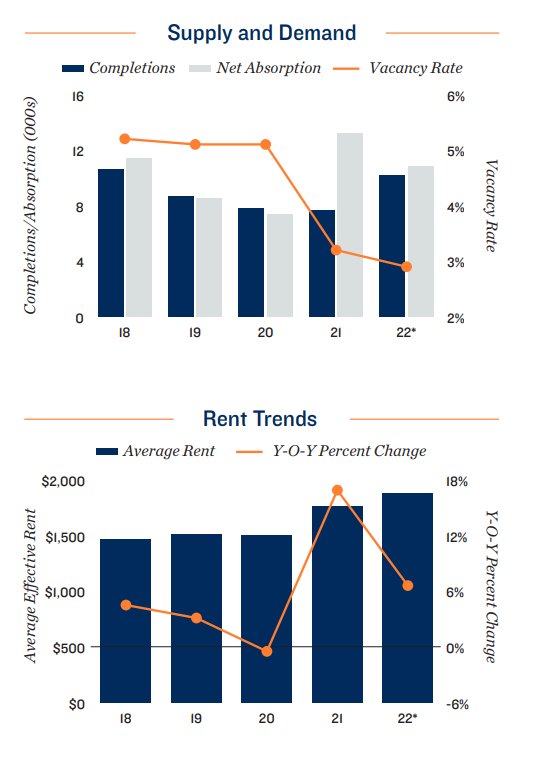

Growing tech scene a boon for Class A demand. Denver’s tech sector is swelling, propelling the market’s median household income above any metros outside of the Bay Area and the nation’s capital. Additionally, the metro’s median age lands 1.6 years below the national average, a positive for rental demand as the 20-34 age cohort is more likely to rent. A young populace with high incomes is translating to low availability of luxury apartments, allowing for strong rent growth. Meanwhile, rates for units toward the lower end of the class spectrum are also on an upward trajectory. The typical gap between Class A and Class C effective rents in Denver is just under $600 per month, and will likely hold in that range. As such, exceptional Class A rent growth will continue to pull up other segments’ rates alongside.

Trendy, urban locales the epicenter of recent demand surge. The metro’s central districts have recorded the strongest drops in vacancy of late — a reversal of the early pandemic trends. Downtown and adjacent submarkets, such as Five Points-Capitol Hill-Cherry Creek, recorded vacancy retreats of at least 270 basis points last year, as renters eagerly returned to the rapidly rejuvenating communities. Notably, improving fundamentals in the CBD have not affected performance in the suburbs. Areas like Broomfield, Littleton and Glendale continue to note vacancy compression. Only one submarket, Southeast Aurora-East Arapahoe County, has a vacancy rate above 4 percent.

Investment Highlights

Denver’s multifamily investment market is one of the strongest in the country, with many foreign and institutional investors expanding in the metro. The fourth quarter of 2021 reported the highest quarterly dollar volume on record, with nearly $4.5 billion transacting. All apartment tiers posted upticks in trading.

Investors have ramped up acquisitions in Downtown Denver; however, a notable increase has also been reported in the metro’s Eastern and Southeastern suburbs. Growing areas like East Denver and Aurora have enticed investors, particularly near light rail stations. Additionally, the southeast, from Glendale to Lone Tree, has reported elevated trading. These areas stand to benefit from a return to offices, as demand for housing near DTC should improve upon workers returning.

Per-unit sale prices have steadily grown in the metro since 2010, with each year showing at least a 7.5 percent increase annually over that stretch. Institutions have become very active in the city, which has raised the metro’s visibility among capital sources and compressed the average cap rate to just under 5 percent. First-year yields as low as 3 percent are not uncommon for top-tier assets in and near the core.

Denver Office:

Adam Lewis Vice President, Regional Manager

Tel: (303) 328-2000 | adam.lewis@marcusmillichap.com

Prepared and Edited By:

Benjamin Kunde Research Analyst | Research Services

For Information on national multifamily trends, contact:

John Chang Senior Vice President, National Director | Research Services

Tel: (602) 707-9700 | john.chang@marcusmillichap.com

The information contained in this report was obtained from sources deemed to be reliable. Every effort was made to obtain accurate and complete information; however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or reliability of the information contained herein. Note: Metro-level employment growth is calculated based on the last month of the quarter/year. Sales data includes transactions sold for $1 million or greater unless otherwise noted. This is not intended to be a forecast of future events and this is not a guaranty regarding a future event. This is not intended to provide specific investment advice and should not be considered as investment advice. Sources: Marcus & Millichap Research Services; Bureau of Labor Statistics; CoStar Group, Inc.; Real Capital Analytics; RealPage, Inc. © Marcus & Millichap 2021 | www.MarcusMillichap.com